By Donna Puncher CeMAP Introduction When choosing a mortgage, one of the most important decisions you’ll make is…

Published: March 20, 2017

BREXIT – How will it affect your finances

The full article can be read here.

If you want to know what happens when a country leaves the European Union, you might as well ask the Inuit.

In one respect, I mean that seriously.

Greenland is the only other country ever to have left the EU – or the European Economic Community (EEC) as it was back in 1985.

Residents of Greenland – including the Inuit – appear to have done well out of leaving, but then their only export is fish.

So can residents of the UK expect to net similar gains, or are our personal finances destined for the deep freeze?

The Pound

The most helpful tool for economic ball-gazers is the value of sterling. Most of them expect the value of the pound to take a significant hit in the medium term. It certainly fell sharply as it emerged that the UK was to leave the EU – at one stage down 10% to its lowest level since 1985.

That is likely to mean:

- buying goods or services from other countries will become more expensive

- inflation will therefore be higher

- goods being sold to other countries will become cheaper for the buyers

So what, in turn, will that mean for our household finances?

Mortgages

Before the vote the Treasury predicted a vote for Brexit would mean a rise of between 0.7% and 1.1% in borrowing costs (on top of what happens anyway), with the prime minister claiming the average cost of a mortgage could increase by up to £1,000 a year.

A rise in interest rates would also affect those in rented accommodation, as costs for landlords would go up.

But amid fears that the vote for Brexit heralds a period of low growth, some economists are suggesting the Bank of England will cut interest rates. In which case, the cost of lending could actually fall.

David Tinsley, UK economist at UBS, said he expects two rate cuts from the Bank of England over the next six months, taking interest rates from a current record low of 0.5% to zero.

House prices

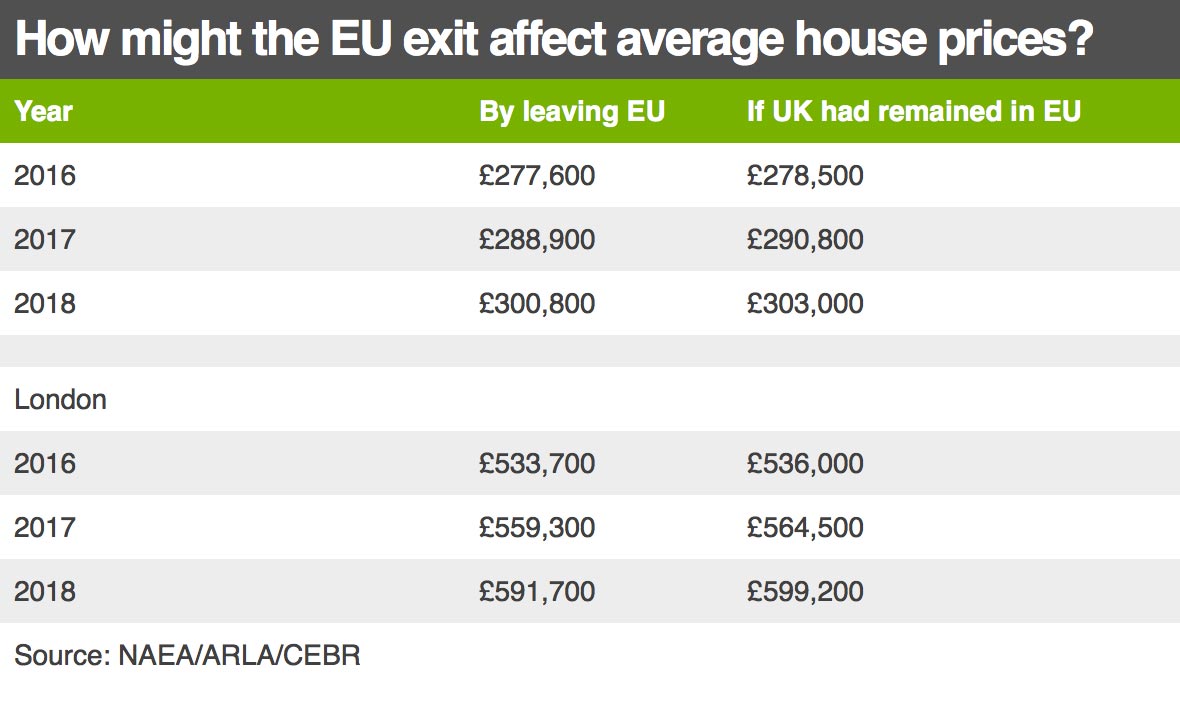

The International Monetary Fund (IMF) has warned that Brexit could cause a sharp drop in house prices. This was on the expectation that the cost of mortgages would rise.

The Treasury has said house prices could be hit by between 10% and 18% over the next two years, compared to where they otherwise would have been. This would be good news for first-time buyers, but not so great for existing homeowners.

The National Association of Estate Agents (NAEA) believes house prices in London could see the biggest change, losing up to £7,500 on average over the next three years, compared to where they otherwise would have been. Elsewhere, it said values could fall by £2,300. But since it expects prices to continue rising anyway, this means a slower rate of increase, rather than a fall in real values (see table below).

And again, if the Bank of England were forced to cut rates, all these projections would be wrong.

Wages

Several experts have predicted that the economic shock of leaving the EU would cause unemployment to rise in the UK. That would reduce the pressure for wage growth. The Treasury estimated that wages will be between 2.8% and 4% lower at the point of maximum impact, with a typical worker at least £780 a year worse off.

But let us not forget that the UK will remain a member of the EU for at least another two years, and predicting economic performance in two years’ time is – even in normal circumstances – notoriously difficult.

Tax

A week before the referendum, George Osborne warned that a vote to leave the EU might result in tax increases too. He spoke about a 2p rise on the basic tax rate – currently 20p in the pound – and a 3p rise in the higher rate – currently 40p. He also said Inheritance Tax (IHT) might rise by 5p, from its current 40p.

But to do so would go against the Conservative government’s promises at the last election, so would be difficult politically.

Many people believe the government would be much more likely to extend the period of austerity beyond 2020. The Institute for Fiscal Studies (IFS) has said that spending might need to be curbed for two further years.

During the referendum the Vote Leave campaign said it wanted to remove the 5% VAT charge on domestic fuel that is currently required by the EU. But it is not clear how – or when – that could be achieved.

Investments and savings

Any rise in interest rates would be good news for savers.

But during the campaign, the Treasury argued that UK shares would become less attractive to foreign investors should we leave the EU, and would therefore decline in value.

In the longer term, this is by no means a certainty. Shares typically rise with company profits. Big exporters might benefit from the weaker pound, so the value of their shares might well rise, while importers might see profits squeezed.

The big investment platform Hargreaves Lansdown has told its clients that it is impossible to know the long-term economic implications of Brexit.

“We cannot assume an Out vote will be bad for the long-term prospects of the stock market,” it said.